With soaring property values across the state, many North Carolinians are struggling to keep up with their housing costs, including property taxes. But there is help. Property tax relief is available for low-income elderly, disabled individuals and disabled veterans. Qualifying owners may receive an exclusion of the taxable value of their residence of either $25,000 or 50% (whichever is greater) but they must apply before June 1, 2025.

Who is eligible?

Qualifying owners must meet the following requirements:

The applicant’s name must be on the deed or title to the residence as of January 1, 2024

The residence must be the applicant’s primary residence.

The applicant must be a North Carolina resident.

The applicant must be at least 65 years of age or totally and permanently disabled. (Total and permanent disability is a disability that substantially hinders a person from obtaining gainful employment.)

The applicant’s income, including any spouse in the household, must be $37,900 or less for 2024.

What if I am a Veteran?

Property tax relief is also available for Disabled Veterans in Mecklenburg County. These qualifying homeowners may receive an exclusion of the first $45,000 of the taxable value of their residence. The veteran must be an honorably discharged veteran, the home must be occupied by the disabled veteran, and that veteran must be 100% totally and permanently disabled due to a service-connected related injury.

This exemption is also available to the surviving spouse (who has not remarried) of a Disabled Veteran. This does not apply to combat veterans, unless they have suffered a 100% total and permanent disability, which is service related. There is no age or income limitation.

When do I apply?

Qualifying owners must apply with the Assessor’s Office between January 1st and June 1st.

Where can I find help?

Charlotte Center for Legal Advocacy is available to assist low-income elderly, disabled, and/or disabled veteran residents prepare their NC property tax relief applications. Click here for more information. Call 980-256-7952 to schedule an appointment.

“I want to move forward.”-Renita shares how she nearly lost her home and the stability the Advocacy Center was able to help her secure.

Posted on

Renita is quick to acknowledge the crucial role faith has played in her life.

“I have been through so much, but I have always had faith that God would see me through it. Whenever I faced obstacles, he seemed to put the right people in my path.”

Her strong faith and personal determination helped her persevere when she nearly lost her home.

Renita lived with her elderly mother until her mother passed away. The oldest of five children, Renita was the only sibling at the time without a stable home of her own. Her mother wanted Renita to inherit the home they shared.

“It was important to my mom that I have a place to call my own and my siblings were very supportive.”

Renita diligently took over the mortgage payments of the house, working long hours to ensure she could stay in the home. But when she was contacted by a scam mortgage assistance firm in 2019, the company convinced Renita to send the mortgage payments directly to them. The fraud continued for 6 months, causing Renita to fall behind on her mortgage. After losing her job at the onset of the pandemic and unable to recoup the payments from which she was frauded, Renita’s home entered foreclosure. Renita was unsure of what to do next and was referred to Charlotte Center for Legal Advocacy.

“From my first phone call with the Advocacy Center, I felt reassured that we would figure out a solution.”

Leah Kane, Consumer Protection Program Senior Attorney, worked with Renita to officially deed the home in Renita’s name and defend against the foreclosure action. The Advocacy Center also helped Renita apply for financial assistance through the COVID-related Housing Assistance Fund (HAF). Once Renita was approved for funding, the Advocacy Center was able to argue in favor of withdrawing the foreclosure case entirely.

“I thank God for the help that was provided and what Leah was able to do. She was so patient and helpful. If I had lost my home, I would have had to move in with my daughter or find somewhere else to live.”

The affordable housing crisis in Charlotte and the surrounding areas would have made finding another place to live difficult. Because Renita’s home has been in her family for nearly 30 years, it is known as a naturally occurring affordable home (NOAH). Ensuring homeowners like Renita can stay in their homes is essential to building a more sustainable community and allowing families to build generational wealth.

Renita’s gratitude for the Advocacy Center is effervescent, but when talking to her, one cannot help but be grateful for her in return. Although she is approaching retirement age, she works 12-hour shifts, 6 days a week, fiercely determined that she will not lose her home.

“I want to move forward. Losing my house would have meant going backward. I’ve worked too hard for that to happen.”

Protect yourself from holiday scams

Posted on

‘Tis the season for holiday scams! We share some helpful tips on common scams and how to protect yourself.

Shopping Online

The two most prevalent scams when shopping online:

Non-delivery scam where a buyer pays for goods or services they find online, but those items are never received, and

Non-payment scam involves goods or services being shipped, but the seller is never paid.

What to Do

Call your credit card company or you bank. Dispute any suspicious charges.

Report the scam to the FBI’s Internet Crime Complaint Center (IC3) at ic3.gov and Contact NC Attorney General’s Office 1-877-5-NO-SCAM or file an online complaint

Use good cybersecurity hygiene: DON’T click on links in emails, websites, or social media. Go directly to the website yourself from a browser like chrome or edge.

Be Careful How You Pay for Items Online or By Phone

Never wire money directly to seller or load money onto “pre-paid” gift cards. This is how scammers typically want payment and the money is often not recoverable. Use a credit card or protected bank debit card if you do not have a credit card, check statements, dispute with your bank. Gift cards are to give for gifts, not to make payments to another.

Gift Card Scams

Scammers want you to pay with gift cards because they’re like cash: once you use a gift card, the money on it is gone. But what do gift card scams look like?

Someone may call, tell you they’re from a government agency, and say you owe taxes or a fine. Or they may pretend to be a family member or friend in trouble, who needs money right away. Or they may say you’ve won a prize, but first must pay fees or other charges. Here are signs you’re dealing with a scammer:

The caller says it’s urgent. They tell you to pay right away or something terrible will happen. They try to pressure you into acting quickly, so you don’t have time to think or talk to someone you trust. Don’t pay. It’s a scam.

The caller usually tells you which gift card to buy. They might tell you to put money on a Google Play, Target, or iTunes gift card — or send you to a specific store like Walmart, Target, or CVS. Sometimes they tell you to buy cards at several stores, so cashiers won’t get suspicious. If so, stop. It’s a scam.

The caller asks you for the gift card number and PIN. The scammer uses that information to get the money you’ve loaded on the card. Don’t give them those numbers. It’s a scam. You’ll lose your money, and you won’t be able to get it back.

Scammers know people receive unexpected packages this season and will send realistic-looking delivery failure notifications so you’ll follow up and reveal personal info. Before you hand over information on the internet, head to your local post office or call the delivery service to verify the notification. These notices can be by fake email or door hangers.

Avoid Holiday Job Scams

To keep your money and personal information to yourself, follow these steps:

Don’t pay to get the job. Scammers may promise you a job — if you pay them. But no legitimate job will make you pay for expenses or fees to get the job. Anyone who does is a scammer.

Never give personal info up front. Some scammers will try to get your credit card, bank account, or Social Security number as soon as you’re in contact.

See what others are saying. Search online for the name of the company plus the words “review,” “complaint,” or “scam.” You might find they’ve scammed other people.

Talk to someone you trust — before you take a job offer or business opportunity. What do they think?

Fake charities

These crop during major disasters and around the holidays. Leaflets and phone calls from organizations with familiar-sounding names will ask you to open your wallets for a good cause. To be safe, don’t give to any charity with whom you didn’t start the contact. Check legitimacy through the North Carolina Secretary of State, Charity Watch, or Charity Navigator.

Beware of “person in need” and grandparent scams.

Scammers pose as a grandchild, friend or relative stranded or otherwise in trouble and need money quickly and quietly. They may ask for money by mail or gift card. Don’t be pressured, hang up and call another relative or friend if you are still concerned to help you investigate.

Old school pickpocketing

Crowded malls and shopping centers are havens for pickpockets. To combat this threat, it’s best to wear purses across the body and wallets in front pockets or inside a closed jacket. Consider leaving the house with the bare minimum, like your ID and debit or credit card (the latter which offer fraud protection and security features not available with cash).

Using 2019 data from the IRS, researchers found that out of 275 hospital systems across the country, 227 spent less on community investments or charity care than they got in tax breaks. The deficit totaled more than $18 billion, the report said.

Leah Kane is a senior attorney for consumer protection at Charlotte Center for Legal Advocacy, a nonprofit that provides civil legal assistance to people who cannot afford an attorney. She said her agency receives calls from people who were not offered charity care from hospitals.

She said her group is worried that hospitals are offering charity care to uninsured patients but not to other people, like the underinsured, who don’t have the income to pay thousands of dollars for treatment not covered by their insurance plans.

“People are angry and stressed out,” Kane said. “They don’t know what this [debt] will mean for their lives.”

No Surprises Act: Protecting patients from surprise medical bills

Posted on

The No Surprises Act protects people from “surprise medical bills.” These protections apply to anyone enrolled in a private health insurance plan, including employer plans or a plan purchased on or off the marketplace. New protections were added in 2022 to restrict excessive out-of-pocket costs from emergency and non-emergency services. If you’re uninsured or you decide not to use your health insurance, these protections allow you to get a good faith estimate of the cost of your care up front, before your visit. If you disagree with your bill, you may be able to dispute the charges.

Even though surprise bills are now banned in many circumstances, enrollees should monitor their medical bills because they might need to take action to protect their rights. Note: Most of the law’s protections only apply to people with private insurance, and not to people who are uninsured or enrolled in Medicaid, CHIP, or Medicare.

New protections for insured patients

The new law protects insured people in two major ways:

For emergency care: An insured person can get care at any emergency department, even if the care is out of network. The out-of-network emergency facility, and the doctors and other providers who treat the patient, cannot bill the patient for more than in-network cost-sharing amounts (i.e., deductible, copay, coinsurance). The plan also must apply only in-network cost-sharing.

For non-emergency care: If the insured person goes to an in-network facility, they cannot be billed for more than the in-network cost-sharing amount for their services, even if they receive care from an out-of-network provider.

Note: Out-of-network ambulance services are not covered by the No Surprises Act and can still lead to high bills.

Key terms

In-network providers: Facilities and doctors who contract to accept a payment rate with your insurer. In-network care generally costs less than care that is out-of-network. You might still have to meet a deductible before your insurance pays the bill, or you might owe a copayment or coinsurance, depending on the type of service and your health plan.

Out-of-network providers: Providers who do not contract with your insurer and instead charge you separately for their services. Unlike in-network providers, out-of-network providers set their own charges. Your health plan might cover some of the cost but often covers none of the cost of out-of-network services.

Surprise medical bill: An out-of-network medical bill a person receives from an out-of-network provider for emergency services, or for non-emergency care while at an in-network facility.

Frequently Asked Questions

What is a surprise medical bill?

Generally, people enrolled in private insurance are responsible for checking their plan’s network before getting health services to ensure that the medical provider they’ve selected is in-network. In most situations, people who get medical services from an out-of-network provider are responsible for paying the out-of-network medical bills they receive. Most plans pay less for out-of-network care than they would pay for in-network care, and some don’t cover out-of-network bills at all, leaving the enrollee responsible for paying most or all the out-of-network bill.

There are some situations where a person doesn’t get to choose their medical provider and ends up receiving out-of-network care. This can happen in medical emergencies when people are taken to the closest ER. It can also happen when people select an in-network hospital for scheduled care but receive care from an out-of-network doctor they did not get to pick (such as the anesthesiologist). These scenarios are common. An out-of-network medical bill a person receives after getting care from an out-of-network provider they didn’t get to choose is known as a surprise medical bill.

What are the new protections if I don’t have health insurance or choose not to use it?

If you don’t have insurance or choose not to use it, these new rules make sure you get a “good faith estimate” of how much your care will cost, before you get care. They also allow you to file a dispute if you are charged more than $400 above the estimate.

What out-of-network providers and services must follow the new law?

Any health care provider in any emergency department or at the insured person’s in-network facility must follow the new law. A “provider” is defined broadly to include doctors, radiologists, therapists, and others. Services like imaging and lab work, preoperative and postoperative services, telemedicine, and equipment and devices are also covered. “Facilities” are hospitals, hospital outpatient departments, and ambulatory surgery centers. They don’t include other settings, such as urgent care.

What should I do if I receive a surprise medical bill?

The first step is to check with the insurance company to see if the provider made a mistake. The out-of-network provider shouldn’t bill for more than the in-network cost-sharing amount for the service(s) indicated on the Explanation of Benefits (EOB). If there is no EOB it might mean that the provider didn’t contact the insurance company as required.

The second step is to contact the out-of-network provider and ask them to correct the bill. Providers can face fines up to $10,000 per violation for not following the new rules.

If the provider refuses to resolve the issue by correcting the bill, then it might be necessary to file a complaint by calling the No Surprises Help Desk at 1-800-985-3059. The No Surprises Help Desk is also available for people who have questions or want more information about the new rules. Consumers can also file complaints online at www.cms.gov/nosurprises.

A mistake made by a person’s insurance company could also result in a surprise medical bill. If that happens, the person should call their insurance company, explain the situation, and ask them to treat the claim as a surprise medical bill. If the insurance company doesn’t correct the issue, the next step is to file an appeal with the insurance company. If this is unsuccessful, the next step is to request an external appeal.

Note: Every EOB a person receives is required to include instructions for how to file an appeal.

What out-of-network providers and services are not covered by the new law?

Services that are scheduled in advance directly with an out-of-network provider are not covered under the new law, and the provider can charge patients the full cost for services.

Are all high medical bills considered surprise bills?

Cost-sharing charges can vary widely across insurance plans, which means that a person could still receive very high medical bills due to their plan’s standard in-network cost-sharing charges being high. These kinds of bills are not considered surprise medical bills.

More Resources:

No Surprises Act, Centers for Medicare and Medicaid Services (CMS)

The holiday season is busy and stressful for many workers, especially hourly workers in the retail, food service, and delivery sectors. During this busy time, employers are less likely to pay workers for all hours worked or to pay overtime rates. It is important for workers to understand common practices that result in unpaid wages and incorrect hourly rates, also referred to as wage theft.

What to look out for

According to the US Department of Labor, common employment law violations during the holiday season include:

Misclassifying employees as independent contractors to evade liability under employment laws

Failing to pay salespeople and cashiers for time spent prepping or closing out registers

Requiring stock room and warehouse workers to work through breaks without pay

Requiring workers to clean or perform closing duties after they have clocked out

Failing to pay promised holiday rates or overtime rates

Who is at risk

Temporary holiday and seasonal workers are particularly vulnerable to wage theft. Employers count on these temporary workers to be unfamiliar with their employment rights and too busy to keep careful track of hours worked. Many temporary or seasonal workers are hired through subcontracted companies or temporary staffing firms, making it even more difficult to track down unpaid wages after the holiday rush is over.

What to do

If you think that your employer isn’t paying you proper wages for all hours worked, it is important to keep records of your pay and hours. Make sure to keep any records of agreed upon pay rates, paystubs, and actual hours worked. It is also a good idea to keep records of any communication with your employer, manager, or supervisor regarding your schedule, hours worked, and pay rates. Pay close attention to any differences between promised overtime or holiday pay and the amount you are actually paid.

The US Department of Labor has a free smartphone app to help workers track their hours.

Learn more

You can learn more about your workplace rights in North Carolina by calling the North Carolina Department of Labor’s Wage and Hour Bureau at 1-800-625-2267 (1-800-NC-LABOR). You can also file a Wage Complaint with the Wage and Hour Bureau; more information is available on the NCDOL website.

If you would like to discuss possible unpaid wages, call us at 704-376-1600.

Beware of COVID-19 Foreclosure Rescue and Forbearance Assistance Scams

Posted on

By Niayai Lavien

Many homeowners are facing increased financial hardships due to unemployment and COVID-19. Scammers are taking advantage of the current economic fallout of the pandemic and employing elaborate scams to trick homeowners out of their properties. Older adults and the economically disadvantaged are more likely to be targets of these abusive practices.

The CDC’s federal eviction and foreclosure moratorium ends on July 31, 2021. The moratorium allows individuals and families living in federally financed properties to stay in their homes throughout the entirety of the COVID-19 pandemic. It also allows families to receive financial assistance to stay current on their rent and mortgage payments.

With the moratorium ending, consumers, especially homeowners, should know their options and learn how to prevent themselves from being scammed.

A foreclosure rescue scam is when a scammer tricks a homeowner into signing away ownership of their home for dramatically less than its current worth. Scammers often target homeowners who are in the middle of foreclosure by promising that they can stop a foreclosure from happening while hiding the fact that the homeowner is signing over title to the property.

Scammers search public records to prey on homeowners who are in danger of foreclosure through failure to pay property taxes, mortgage or homeowners association dues. They also look for older homeowners who have paid off their mortgage, but have trouble with the financial upkeep of their home.

Common abusive practices include:

Aggressive solicitation via phone, text message, mail and door hangers

Downplaying the value of the home

Pressure to sign a document or contract without the presence of a Realtor or attorney

Whatever the particular factors surrounding a homeowner’s situation, the scammer’s goal is to steal the home’s dollar while a person is in a high pressure situation.

Do’s and Don’ts of Foreclosure Scams:

Don’t → Fall for unsolicited offers to buy your home or help you sell your home without any cost.

Don’t → Make a decision regarding your home without getting a second opinion.

Don’t → Be pressured into signing any papers until you’ve talked with an attorney.

Do → Consult with a HUD approved counseling agency to talk about your options.

Do → Be wary of out-of-state law firms, organizations and groups offering to provide assistance.

Do → Contact Charlotte Center for Legal Advocacy’s Consumer Protection Team for assistance at 704-376-1600.

Responding to Crisis: Marking One Year of COVID-19

Posted on

Last March, few imagined that our community would still be grappling with the coronavirus pandemic a year later.

In many ways it seems the pandemic is nearing an end after this year of hardship and loss: vaccines for the virus are increasingly available, and cases have dropped to a point where North Carolina is easing activity restrictions.

But we are only just beginning to understand the extent to which this virus has driven our neighbors to the margins of safety, economic security and family stability, laying bare the extreme inequities that have long existed in our community.

Charlotte Center for Legal Advocacy has spent the last year fighting for our community’s most vulnerable residents as COVID-19 upended daily life.

As we pass this milestone, we take stock of just how much we’ve fought to advance our mission of pursuing justice this past year.

It’s work we do every day and have always done in our 50+ years of service. But COVID-19 has cast a glaring spotlight on the importance of our mission.

Pursuing justice: It’s fairness under the law. It’s equal access. It’s meeting basic needs. And it’s making sure our neighbors are equipped to endure any crisis life throws their way, including a global pandemic.

Today and every day, we continue this hard, necessary work until our community is a stronger, more just and equitable place for ALL.

Over the past year we:

Addressed immediate issues related to agency closures in our local Department of Social Services (DSS), allowing for remote application for benefits and limiting terminations and state unemployment insurance systems to tackle issues stalling federal unemployment benefits.

Prevented illegal evictions and kept vulnerable populations safely housed.

Responded to critical needs for protective orders and intervention due to a sharp increase in domestic violence incidents while our courts were operating on a limited capacity.

Monitored the changes in Medicaid, food stamps and other assistance programs to ensure coverage is not disrupted for those who need them in our community.

Advocated for language and technological access on administrative applications for health, food and income benefits to ensure all who were entitled to assistance could receive it.

Assisted people who have lost their jobs and/or health insurance navigate Affordable Care Act health coverage options and Special Enrollment Periods (SEPs).

Ensured members of our community are not falling victim to COVID-19 related scams and losing their income.

Helped immigrant families understand the unique ways the pandemic impacts employment, housing, public resources, ICE activity and immigration courts.

Read on to learn more about the need for our services and our impact over the past year.

Meeting Exacerbated Needs

Days after the first cases were reported, we shifted to remote operations, equipping staff to continue our work as the need for help grew exponentially.

For our neighbors living on economic and health margins, the pandemic has further exacerbated their instability in extreme ways.

The need for our services before the pandemic:

More than two thirds of low-income households were experiencing at least one civil legal problem that significantly impacted daily life. These rates are much higher for survivors of domestic violence, immigrants, veterans, families, and parents of children with disabilities.

In Mecklenburg County, poverty, segregation, and income inequality have pushed residents to the sidelines, concentrating distress in family stability and fortifying barriers to economic opportunity.

Children born into poor families in Mecklenburg County are among the least likely in the U.S. to escape poverty.

Public agencies closed and delayed services just as newly unemployed individuals found themselves trying to piece together a semblance of stability navigating administrative and public benefits systems for the first time.

Those already depending on these systems (people with disabilities, children, seniors, veterans and their families) were desperate to prevent the illness, hunger and homelessness that could result from losing Medicaid, Food Stamps, Social Security, Supplemental Security Income (SSI) or other benefits.

The combined effects of racial, gender, ethnic, and other forms of bias create multiple barriers for people of color and women as they navigate institutions where entrenched disparities remain the status quo.

This clear intersectionality has yielded disproportionately negative impacts for people of color and women during the pandemic. Because of this reality, we have continued to identify and address systemic racism while fighting to ensure equal access to assistance.

When Mecklenburg County’s Department of Social Services (DSS) closed its offices to the public on March 18 with little notice, we fought to make sure our neighbors could still get benefits and services guaranteed to them under the law.

We made DSS agree to:

honor the date of phone calls as date of application for applicants to ensure they receive the maximum amounts of benefits allowed;

not terminate benefits for missed deadlines; and

allow late appeals, and to post clear signage in front of their buildings outlining this information.

The closure sent applicants to the agency’s call center which meant longer wait times for help.

We made sure people understood their eligibility for public benefits, helped them apply and navigate confusing administrative systems, all while ensuring their rights were protected. When programs and services changed, we kept the community informed.

We continue to advocate for extensions and flexibilities that are favorable to beneficiaries, while serving as a watchdog to ensure those policies are appropriately enforced and accessible to applicants of all backgrounds.

‘Things are smoother now.’

Like many of our neighbors, Melody was already struggling when COVID-19 turned her life upside down. We assisted her with various legal needs last year. Recently, we checked in to see how things are going for her and her family one year into the pandemic.

When someone contacts Charlotte Center for Legal Advocacy for help, they are often struggling to stay afloat in a storm of crisis.

They have a big problem impacting their life but do not know how to fix it. Their problem is a symptom of various unmet legal needs that need to be addressed comprehensively to put that person on a better path.

As the primary financial support and caregiver for her family, she was trying to keep up with medical bills and fighting to keep her home as she faced foreclosure for unpaid property taxes from the mid-2000s left over from her parents’ estate.

The Advocacy Center had helped her negotiate a payment plan with the county that included forgiveness of a substantial portion of the debt.

“When the pandemic hit, I lost my job,” Melody says. “I was devastated. I thought, ‘How am I going to make those payments?’”

Melody is used to being the one helping others. But when it came to piecing together the support her family needed to remain stable, she could not do it alone.

Again, she called the Advocacy Center. We connected her with Legal Aid of North Carolina-Charlotte to help her get expanded unemployment benefits under the CARES Act to support her family.

“I’ve worked all my life and never needed any benefits,” Melody says. “I didn’t really know how that stuff went.”

As part of our work, we learned that Melody’s sister, Wendy’s social security benefits had been terminated despite her disability. The Advocacy Center stepped back in to ensure she was receiving the benefits she was entitled to.

We also helped Wendy apply for food stamps to help their family through this crisis. Melody would soon turn 65, so we also ensured everything was prepared for her to receive Medicare in a few short months.

We checked in with Melody recently to see how things are going for her and her family one year into the pandemic.

It’s been hard.

She’s lost eight family members to COVID-19. In addition to not being able to physically mourn with her loved ones, she’s missed the big family get togethers held every year—egg hunts at Easter and a family reunion in September.

Melody says one thing she’s learned through her experience is “it’s okay to ask for help and it’s okay to not be okay.”

She compares the past year to sailing through a storm and credits the staff at the Advocacy Center for guiding her to calmer waters.

“Just knowing I had them there, I was able to stay in my boat,” she says. “Things are smoother now.”

Despite the past year, she says she is still looking for the silver lining in everything.

She hopes to return to her job whipping up the daily special at Showmars in the City of Charlotte Government Center, where she had worked for 22 years. And she dreams of one day owning her own food truck.

In the meantime, she’s glad to have her health, her family cared for and a place to call if she needs help.

She smiles every time she drives by the Advocacy Center and Legal Aid office on Elizabeth Avenue.

“Look at how much work the people in that teeny little building do!” Melody says. “The work they do, it’s needed. Because sometimes people just need a helping hand. It’s been a blessing.”

Melody, we’re glad we could help. Call us if you need anything.

Before the pandemic, about 12 percent of Mecklenburg residents, including children, were considered food insecure according to Feeding America. The ongoing economic fallout has swollen that number to almost 16 percent who are on the brink of hunger.

In the last year, our staff assisted 371 people and their families with issues accessing food stamps (SNAP benefits), making sure they could successfully get the assistance they needed to remain stable and understood their eligibility for SNAP and other public benefits.

North Carolina was among the earliest adopters of Pandemic EBT (PEBT), which provides food support for families with children eligible for free or reduced-price meals while schools were closed. Though N.C. took many positive steps in creating this program, there have been hurdles and confusion in the implementation. We have been working closely with clients, partner organizations, and the state to monitor issues on the ground and communicate them to N.C. Department of Health and Human Services to ensure the program works efficiently and families receive these critical benefits quickly.

Healthcare Access

Our health insurance navigators and call-back volunteers assisted over 1000 community members apply and select an affordable health insurance plan for their budget during Open Enrollment Nov. 1 – Dec. 15. Health insurance is critical to safety, stability, and health–particularly during the COVID-19 crisis.

Before the pandemic, one in six Americans had a civil legal problem that negatively impacted their health. We knew that unmet legal needs related to COVID-19 would dramatically worsen health outcomes.

Thirteen percent of Mecklenburg residents don’t have health coverage. More than 500,000 low-income people in N.C. have no options to get health care because they earn too much to qualify for Medicaid and too little to receive financial assistance for health insurance.

COVID-19 forced frontline workers to weigh the risks of working to keep their families stable with the chance of falling critically ill and needing to seek medical care they couldn’t afford. Others lost health insurance benefits with their jobs at a time when access to health care mattered most.

Many who lost their jobs due to COVID-19 did not realize they had the option to apply for health care coverage through a Healthcare Insurance Marketplace Special Enrollment Period (SEP) 60 days after losing coverage. Consequently, many went without it due to their inability to afford private insurance.

Johanna Parra, coordinator of the Advocacy Center’s Health Insurance Navigator Project, was among the first in the nation to discover another option for those who were desperate to get coverage and have peace of mind knowing they could get care if they needed it.

Because all 50 states were under the COVID-19 pandemic national emergency declaration, eligible individuals could apply for coverage through the Affordable Care Act’s Health Insurance Marketplace, also referred to as “Obamacare,” for a Special Enrollment Period through the Federal Emergency Management Agency (FEMA SEP).

Fighting for Equal Access

As soon as Congress passed the CARES Act to provide economic support and COVID-19 relief, there was confusion around the benefits included in the package.

Understanding the CARES Act and COVID Relief: Stimulus Payments and Unemployment Benefits

Families desperate for financial support needed help making sure they received stimulus checks (Economic Impact Payments) issued by the federal government.

Who was eligible? How would payments be distributed? What if payments didn’t arrive?

We answered these questions and more for our clients and the community to ensure everyone eligible for a payment could receive it.

Staff are now helping people address missing stimulus checks and other issues related to the CARES Act as people try to prepare their 2020 tax returns at a time when collection activities and massive job losses strain taxpayers. We are working to resolve these issues and push the IRS to offer specific remedies for various issues related to stimulus checks.

We are also working closely with clients and partner organizations to ensure the latest COVID-19 stimulus opportunities from the American Rescue Plan are understood and correctly received.

By May of last year, more than one million North Carolinians had applied for unemployment insurance benefits. The volume of applications paired with implementing new assistance programs under the federal CARES Act has caused significant delays, making the process more challenging for applicants.

Working together, Charlotte Center for Legal Advocacy and Legal Aid of North Carolina-Charlotte answered the calls of thousands of frustrated workers to guide them through the application process and appeals. Through direct action and systemic advocacy, these organizations ensured that those who had fallen through the cracks had access to the full payments they deserved.

Prior to the pandemic and historically, North Carolina’s unemployment system made it difficult for eligible residents to receive unemployment benefits, leaving workers with little to no support.

Charlotte Center for Legal Advocacy is focused on removing some of these barriers by focusing on unemployment insurance system reform, essential worker benefits, living wages, and promoting workers’ rights in a right to work state—all of which disproportionately impact People of Color (POC).

We are also monitoring how scams and multi-level marketing schemes (MLMs) target unemployed and low-income individuals, especially during the COVID-19 crisis.

NC Extra Credit Grant

The NC Extra Credit Grant program provides financial support for families struggling to meet the demands of educating and caring for their children during the COVID-19 pandemic. For a parent living on minimum wage, $335 is more than he or she will earn in a week. We worked to spread the word to make sure that families who missed the first deadline didn’t miss this final application period and the chance at financial assistance.

Quick action and a strong partnership generated 24,946 applications submitted; $8 million distributed, in just 18 days.

On September 4, Gov. Roy Cooper announced the Extra Credit Grant: an additional $335 dollars in COVID-19 relief for N.C parents. While middle and high-income families automatically received the payment, low-income families had to apply through the North Carolina Department of Revenue (NCDOR).

These families had just 29 days to learn about the program and apply. Only 10,000 families did so during the initial application period.

Through a pro bono partnership, Legal Aid of North Carolina, Charlotte Center for Legal Advocacy, and Robinson Bradshaw filed a complaint resulting in a court order on Nov.5, 2020 that reopened and extended the application period.

Charlotte Center for Legal Advocacy created a website and extensive communication campaign entitled 335 for NC, which encouraged these parents to apply for the grant through December 7, 2020. More than 32,000 individuals visited the website.

In just 18 days, Charlotte Center for Legal Advocacy, Legal Aid of North Carolina, and Robinson Bradshaw reached hundreds of thousands of families and delivered 24,946 applications to NCDOR resulting in more than $8 million in aid made available to families who needed it most.

Keeping Families Safe and Protected from Exploitation

Housing Rights

State and federal moratoriums on evictions and foreclosures have been implemented and continued over the past year to keep people who couldn’t pay their bills safely housed during the pandemic, but they haven’t been enough to protect everyone.

As we watched infection rates rise, courts in North Carolina started working through backlogged foreclosures. Evictions began ramping up, exacerbating the shortage of affordable housing that existed well before the threat of coronavirus. Homeowners who had to take advantage of forbearance because they could not pay their mortgages will eventually have to repay extraordinary balances on their home loans, many of which cannot be modified.

The Advocacy Center continues to work with families desperate to keep their homes and stay current on their bills to avoid homelessness and financial ruin. We are making sure people understand their rights and obligations with lenders to help them make informed decisions about their situations. We are also educating the community to make sure our neighbors do not fall victim to scams related to COVID-19.

‘The weight that was lifted off’

Entrepreneur, grandmother, personal shopper, caregiver, and church activist. These are a few of the hats that Mrs. C wears on any given week. She keeps copious amounts of to-do lists to keep herself, her family, and her business in order, a skill she says she learned from the staff at Charlotte Center for Legal Advocacy.

“I kept their organizational skills, detail-oriented skills and people skills. It was a great learning experience.”

Mrs. C sought Charlotte Center for Legal Advocacy’s assistance when a predatory mortgage company threatened to foreclose on her and her husband’s home.

“Raising grandkids, things got tight, but I also felt like I got hoodwinked into this mortgage. I had an anxiety attack.”

Mrs. C quickly connected with our Consumer Protection Unit which soon found out her mortgage company was fraudulent and under federal investigation. The Advocacy Center resolved Mrs. C’s issue and her family was able to keep her home.

“I cannot tell you the weight that was lifted off me when Charlotte Center for Legal Advocacy jumped in like that and helped me right off the bat. It was a godsend. They worked with me on everything.”

Without the burden of potential foreclosure, Mrs. C can focus on growing her business and fostering her family:

“It’s peaceful now. I’m able to move forward. If only you could see the smile on my face! It’s a peaceful, peaceful smile.”

Immigrant families were already targets for exploitation before the pandemic. Fear of deportation, language barriers, and lack of traditional financial resources make it harder for immigrants to get assistance and leave them vulnerable.

Owners of substandard housing often rent to immigrants because the owners believe those tenants will be afraid to exercise their rights to habitable housing and to continued tenancy.

Traditional financing options are also often unavailable to immigrant families, which makes them easy targets for predatory financing options such as contracts for deed, options to purchase, installment sales contracts or lease with option contracts. These are enforced through eviction procedures and are complicated to defend without legal assistance.

Immigrants are also targeted for predatory sales of mobile homes, which can be substandard. These situations often involve predatory financing methods on land that is rented and are subject to eviction from the land, also requiring complicated defense.

The pandemic hit immigrants especially hard. Primary earners lost jobs as businesses shut down and those without legal status didn’t qualify for COVID-19 assistance.

“Because of the virus we lost our jobs and that put us behind on rent. And now it’s worse because my husband had an accident and our court date is tomorrow so we don’t know what we’re going to do … We don’t get help from anyone, those of us who are undocumented. A lot of us are going through this.”

– Advocacy Center client Ismar spoke to WFAE as her family faced eviction in July. Attorney Juan Hernandez was able to negotiate an agreement with the family’s landlord to prevent them from losing their home. Listen to the full story.

Thinking they could take advantage of families in desperate situations, landlords continued to threaten and illegally remove families from their homes.

At a time when our court system was operating on a limited capacity and resources for assistance were scarce, we helped our clients avoid homelessness, remain stable and exercise their rights.

During the COVID-19 pandemic, Charlotte Center for Legal Advocacy continues to find innovative ways to serve our community. In October, our Immigrant Justice Program partnered with Latin American Coalition to host a “curbside” clinic on the CDC Eviction Moratorium. Over thirty clients attended throughout the day to learn how to claim its protections.

We upheld their rights through our work, which included remedies such as cancellation of the contract, recovery of down payment or money paid above and beyond the fair market rental value, damages for unfair and deceptive trade practices, among others. We also conducted community education programs regarding the rights of immigrant renters related to their housing.

Domestic Violence Protection

While officials urged people to stay home to prevent spreading the virus, home wasn’t the safest option for many in our community.

Immigrant women also face additional barriers to escaping domestic violence or abuse, leaving them feeling trapped in abusive situations.

Charlotte Center for Legal Advocacy helps low-income immigrants living in Mecklenburg County who are victims of domestic violence. A recent Allstate Foundation national survey found that 64 percent of Hispanic women say they know a victim of some type of abuse and 30 percent have personally been victimized.

Reports of domestic violence incidents increased significantly along with the need for legal assistance to get necessary protection early in the pandemic as people. Advocacy Center staff helped survivors and their families navigate administrative changes to get the protections they needed while our courts were closed.

Our Response Continues

We are all weathering the same storm, but we are not all in the same boat.

The past year has made it clear just how critical access to safety, security and stability is for everyone in our community.

But barriers that prevent equal access to these needs persist. And our current safety net is simply not wide or strong enough to support everyone who needs it.

Much like the Great Recession of 2008, the recovery for those hit hardest by COVID-19, those we serve, will take years. Some will never recover.

The need is everywhere. That’s why we’re here, fighting to help families not only stay afloat but also thrive. And we’re not going anywhere.

Today and every day, we continue this hard, necessary work until our community is a stronger, more just and equitable place for ALL.

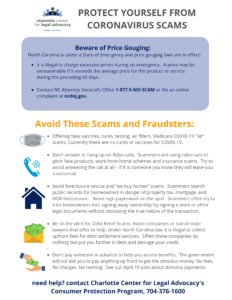

Scammers are always looking to take advantage of unsuspecting victims, especially in times of uncertainty. The more you and loved ones know about scams, the easier it is to spot and avoid them.

Download these tips for protecting yourself from coronavirus scams.

Beware of Price Gouging

North Carolina is under a State of Emergency and price gouging laws are in effect:

It is illegal to charge excessive prices during an emergency. A price may be unreasonable if it exceeds the average price for the product or service during the preceding 60 days.

Contact NC Attorney General’s Office 1-877-5-NO-SCAM or file an online complaint

Tips to Avoid Scammers and Fraudsters

Be aware of COVID-19 vaccine scams. Everyone who wants a vaccine can have one and the vaccine will be free for most people. Learn more about COVID scams here.

Don’t answer or hang up on Robo-calls. Scammers are using robo-calls to pitch fake products, work-from-home schemes and insurance scams. Try to avoid answering the call at all – if it is someone you know they will leave you a voicemail.

Avoid false utility company representatives: Scammers are calling to dupe people out of their cash and personal information by convincing them their utilities will be shut off if they don’t pay. If you get a call from someone claiming to be your utility company, firmly tell them you will contact the utility company directly using the number on your bill or on the company’s website. Even if the caller insists you have a past due bill or your services will be shut off, never give banking information over the phone unless you place the call to a number you know is legitimate. Utility companies neither demand banking information by email or phone nor demand payment by gift cards (like iTunes or Amazon), cash reload cards (like MoneyPak, Vanilla, or Reloadit), or cryptocurrency (like Bitcoin), these are scams.

Avoid foreclosure rescue and “we buy homes” scams. Scammers search public records for homeowners in danger of property tax, mortgage, and HOA foreclosure. Never sign paperwork on the spot. Scammers often try to trick homeowners into signing away ownership by signing a deed or other legal documents without disclosing the true nature of the transaction.

Be on the alert for Debt-Relief Scams. Avoid companies or out-of-state lawyers that offer to help. Under North Carolina law, it is illegal to collect upfront fees for debt settlement services. Often these companies do nothing but put you further in debt and damage your credit.

Don’t pay someone in advance to help you access benefits. The government will not ask you to pay anything up front to get the stimulus money. No fees. No charges. No nothing. See our April 19 post about stimulus payments.

Avoid Social Security scams. The government will not call to ask for your Social Security number, bank account, or credit card number. Anyone who does is a scammer. Don’t “verify” your number or be scared into thinking your benefits are about to be suspended.

Watch out for phishing emails and texts about the coronavirus that appear to be from health officials, experts, or anyone else. Don’t open messages, click on links, or download attachments from senders you don’t recognize.

Be cautious of offers to help get groceries, do errands – there are a number of good Samaritans, but unfortunately there have also been reports of scams, money given, nothing delivered.

Beware of “person in need” and grandparent scams. Scammers pose as a grandchild, friend or relative stranded or otherwise in trouble and need money quickly and quietly. They may ask for money by mail or gift card. Don’t be pressured, hang up and call another relative or friend if you are still concerned to help you investigate.

Be cautious of any unsolicited door-to-door sales pitch or offers. Don’t sign or agree to anything on the spot – if an offer seems too good to be true it probably is.

Still have questions or need help? Contact Charlotte Center for Legal Advocacy’s Consumer Protection Program for more information, 704-376-1600. Stay safe everyone!

Additional Resources

Read more information and report scams through the links below and pass it on:

Student Borrower Advocates Call for Canceling Student Debt to Tackle Economic Fallout

Posted on

Charlotte Center for Legal Advocacy has joined advocates from across the country in calling on Congressional leaders to address student loan debt issues being exacerbated by COVID-19.

Here is the letter addressed to House Speaker Nancy Pelosi, House Minority Leader Kevin McCarthy, Senate Majority Leader Mitch McConnell and Senate Minority Leader Chuck Schumer:

The 66 undersigned community, civil rights, consumer, and student advocacy organizations thank you for taking swift action to pass the CARES Act to begin to grapple with the ongoing economic fallout caused by the coronavirus. However, much more must be done to ensure that student loan borrowers and the economy recover when this crisis ends. We urge you to include student debt cancellation in the next coronavirus package, and for those who will still have federal student debt, to extend suspension of those payments through March 2021.

We are concerned about the increasingly grim predictions we hear about the state of our economy. Without a comprehensive long-term solution, the CARES Act suspension of federal student loans for eighty percent of borrowers merely kicks the problem down the road to this fall, when jobless claims are predicted to exceed Great Depression-era levels, and the financial crisis will have severely deepened. The president of the Federal Reserve Bank of St. Louis, James Bullard, predicted the U.S. unemployment rate may hit 30% in the second quarter, a level five percent greater than was reached during the Great Depression. Goldman Sachs is projecting a record-breaking 24 percent drop in GDP for the second quarter of 2020, and that the world economy is expected to contract by 1 percent this year—which would be a greater worldwide contraction than the one following the 2008 financial crisis. And the downturn is expected to last well beyond this year: Morgan Stanley predicts that GDP in developed markets won’t return to pre-virus levels until the third quarter of 2021.

The student debt relief in the CARES Act fails to address this looming economic crisis. First, the six-month suspension on federally-held federal student loans leaves out an estimated one in five borrowers who owe on commercially-held FFEL loans or Perkins loans. Second, even for the eighty percent of borrowers who benefit from a six-month suspension, many will face the daunting prospect starting in October of choosing between paying for necessities including food, medical care, and rent, or making their student loan payment.

The next stimulus package must take the necessary steps to ensure economic recovery down the line: this means federal student debt cancellation, so the hardest hit don’t struggle, and an extended federal student loan payment suspension that is expanded to all borrowers to at least March 2021, so those who will continue to have payments will have more breathing room to get back on their feet. Without taking these additional steps, the CARES Act sets up millions of federal student loan borrowers to face the daunting prospect of trying to find the means to pay their student loans in the middle of economic devastation.

Cancelling federal student debt would bring impactful relief to 43 million Americans and their families. Loan cancellation would provide the greatest benefit to many struggling low-income borrowers who would likely see their debt extinguished. For those who would still have a balance, suspending payments until the end of the year would prevent them from facing yet another financial shock when the CARES Act federal student loan suspension expires in October. An extended payment suspension would enable many economically distressed borrowers to focus on recovering from a once-in-a-lifetime national emergency and free up extra dollars to inject into the economy. It would also strengthen the finances of student loan borrowers and their families over the long term by ensuring that tens of millions of borrowers come out of this crisis with lighter debt burdens.

In response to the COVID-19 pandemic and its devastating economic impact, it is crucially important to include student loan debt cancellation as a part of any economic stimulus. We support the proposals that Senate and House Democrats have put forward to cancel student debt by establishing a program to make principal and interest payments on outstanding federal student loans throughout the duration of this crisis. Such a program would ensure that loan balances go down throughout the duration of the crisis, putting millions of households in a better position to deal with the long-term economic fallout this crisis will create. We also support the Student Debt Emergency Relief Act by Representatives Ayanna Pressley and Ilhan Omar to cancel a minimum of $30,000 in federal student loans.

Cancelling student debt would ensure that, come fall, borrowers are able to shoulder the ongoing costs of food, supplies, and medications if they, like many workers, face layoffs or smaller paychecks (due to reduced hours or slower business) because of the pandemic. And at a time when student loan servicers are shuttering call centers or reducing capacity, student loan cancellation would ensure there is less need for borrowers to take time out of their days to chase down their servicers and try and secure changes to, or help on, their student loans.

Reports show that cancelling student debt would also boost the economy for everyone in the medium-to-long term. It would boost GDP by up to $108 billion a year, and add up to 1.5 million jobs per year. Research by the National Bureau of Economic Research shows that federal student debt cancellation increases borrowers’ incomes by about $3,000 over a three-year period.

Even before the COVID-19 pandemic, the United States was facing a student debt crisis: outstanding student debt surpassed $1.6 trillion, over 9 million borrowers were in default on their federal student loans, and another borrower goes into default every 26 seconds. The burden of default falls particularly hard on communities of color. Black students must borrow at higher rates and in larger amounts due to racial inequities in incomes and wealth. Additionally, women hold two-thirds of the country’s student debt and on average borrow $3,000 more than men to attend college—yet because of the wealth and wage gap, women find it harder to repay their loans. Three million Americans over the age of 60 still have student debt. More than 40,000 people over 65 have their Social Security payments, tax refunds, or other government payments offset or garnished because they have fallen behind on their student loan payments. According to a Consumer Financial Protection Bureau (“CFPB”) Snapshot report, older borrowers are more likely than those without outstanding student loans to report that they have skipped necessary health care needs such as prescription medicines, doctors’ visits, and dental care because they could not afford it.

Now more than ever, we must ensure that all people prioritize the health and economic wellbeing and that of their families and neighbors. Federal student debt cancellation is an essential factor in making that possible, and we strongly urge you to include this relief in the next COVID-19 package.

Sincerely,

National organizations: Allied Progress American Federation of Teachers Americans for Financial Reform Association of Young Americans (AYA) Center for Digital Democracy Center for Economic Integrity Center for Justice & Democracy Center for Law and Social Policy (CLASP) Center for Responsible Lending Center for Survivor Agency and Justice Consumers for Auto Reliability and Safety Disability Rights Education & Defense Fund (DREDF) Economic Opportunity Institute The Education Trust EMPath Hildreth Institute NAACP National Association of Consumer Advocates National Association of Consumer Bankruptcy Attorneys (NACBA) National Center for Transgender Equality National Consumer Law Center (on behalf of its low-income clients) National Women’s Law Center The Midas Collaborative OCA – Asian Pacific American Advocates Public Citizen Public Justice Center Public Law Center Student Action Student Borrower Protection Center Student Debt Crisis Young Invincibles

State and local groups: ACTION – Allied Communities of Tulsa Inspiring Our Neighborhoods Alaska PIRG Arkansans Against Abusive Payday Lending Arkansas Community Organizations Bucks County Women’s Advocacy Coalition Charlotte Center for Legal Advocacy Convencion Bautista Hispana de Texas Delaware Community Reinvestment Action Council, Inc. East LA Community Corporation Fairbanks Climate Action Coalition Faith Action Network – Washington State Georgians Against Predatory Lending Habitat for Humanity of Anderson County, TN Just-A-Start Corporation Lawrence CommunityWorks Maine Center for Economic Policy Maryland Consumer Rights Coalition Massachusetts Affordable Housing Alliance Massachusetts Education Justice Alliance Michigan League for Public Policy Michigan Poverty Law Program Montana Organizing Project New Jersey Citizen Action New Jersey Tenants Organization PathWays PA Pennsylvania Council of Churches PHENOM (Public Higher Education Network of Massachusetts) Project LIFT SC Appleseed Legal Justice Center Tennessee Citizen Action Tzedek DC Virginia Citizens Consumer Council VOICE OKC Wisconsin Faith Voices for Justice WV Citizen Action Group